Quarterly Newsletter 2026 Q1

The beginning of a new year gives optimism for what might be achieved and concern moving on from the familiar. If we learned anything from last year is that this administration is set on transition.

We can expect large scale changes in foreign affairs. Europe will soon transition to taking responsibility for its own security. Iran will likely transition from a theocracy back to a some form of open government. Venezuela from a tyranny to a democracy. Iceland may transition to United States control. The economy is transitioning into more manufacturing. The list goes on.

Through all of the transitions, we are optimistic about the health and strength of the United States economy. Demand stayed higher than we anticipated last year, and the stock market reflected it. We would not be surprised to see some economic softening in 2026, but the Federal Reserve has plenty of levers to pull to keep the economy on solid footing.

No doubt we will be surprised by something, and when that happens, our clients can rest assure that our Risk Allocation models will take advantage of any opportunity.

2025 4th Quarter Review

In our last newsletter, we discussed not being surprised if we had a market pullback some time during the fourth quarter, and we did. After a strong October, the market declined a bit in November, but finished the quarter positive 2.90%.

We also thought the Federal Reserve was likely to decrease the Federal Lending Rate. The Federal Reserve dropped it twice; .25% on October 30th and again on December 11th.

2026 1st Quarter Preview

The stock market has been relatively calm for several months. We don’t see any obvious reason to believe that will change. Our biggest concern remains high stock prices. In this environment, it may not take much to make the market overreact to negative news. That said, we are optimistic of the first quarter of 2026 and the entire year.

Bonds

Last year was a very good year for high grade bonds. This was not a surprise as high-grade bonds tend to react to interest rate changes more than high yield bonds. We continue to believe interest rates will decrease in 2026 setting up another strong year for high grade bonds.

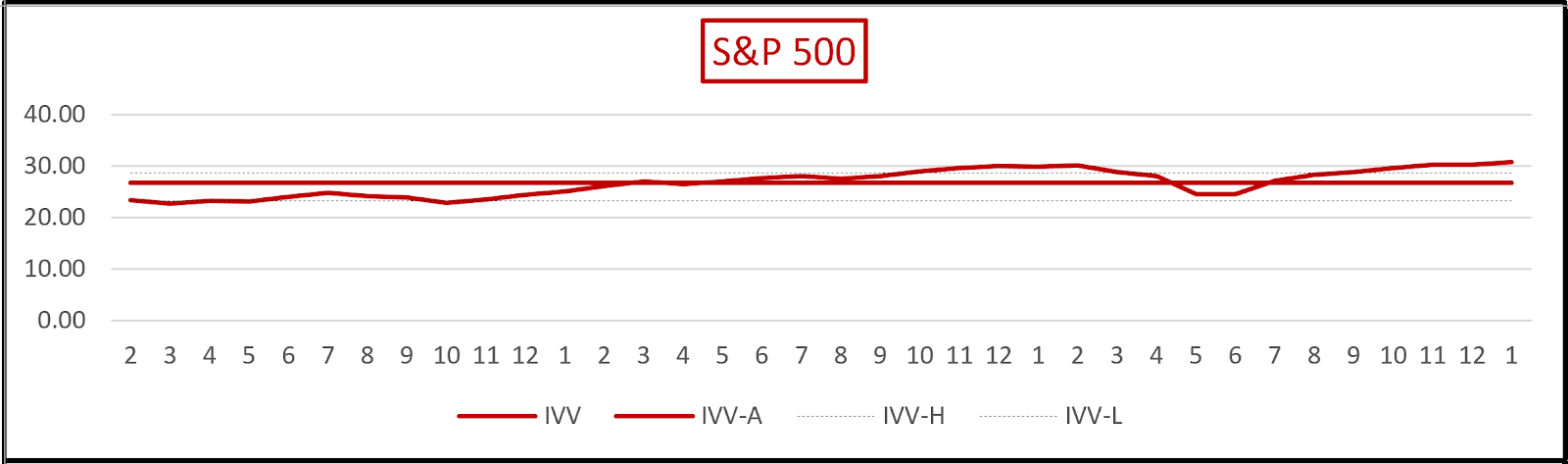

US Stocks

The graph below shows high stock prices relative to earnings. This generally means earnings need to increase or prices could decline. However, there are other reasons stock prices are high. Technology stocks generally have higher price to earnings (P/E) ratios than other sectors of the stock market. As technology companies have become a larger portion of the S&P 500 index, P/E ratios have increased. Also, P/E ratios have increased over the long run. Just because P/E ratios are high does not mean they have to fall any time soon. Therefore, we are still bullish on the stock market for 2026.

International

International stocks a very good year due to high earnings in Europe and Asia coupled with a weaker U.S. dollar. Foreign stocks also started the year with lower valuations than U.S. stocks. These factors could easily continue in 2026. For the first time in several years, international stocks look encouraging. This may be a good time to increase international stock holdings in more aggressive portfolios.

Did You Know?

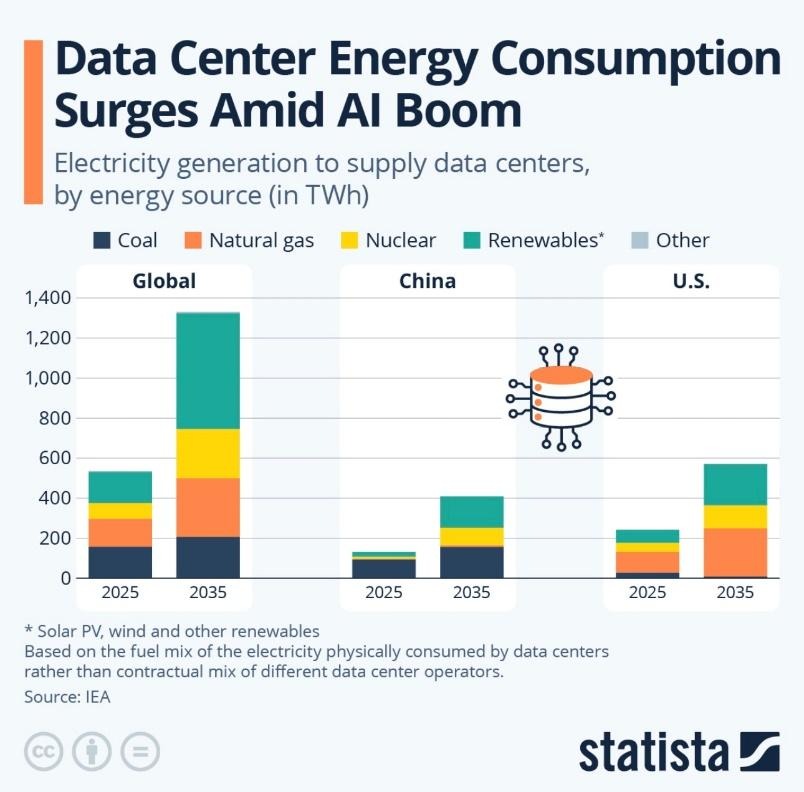

Artificial intelligence is poised to become one of the largest new drivers of global electricity demand, as data centers, cloud computing, and AI training models require vast amounts of constant power.

Regions with strong nuclear, hydro, wind, and solar capacity are better positioned to meet AI’s energy needs while maintaining grid stability and emissions targets.

As AI adoption accelerates, the future competitiveness of economies may depend not just on computing power, but on access to reliable, scalable electricity.

Have you reviewed your retirement strategy this year? We’re here to help.