2025 Q4 Newsletter

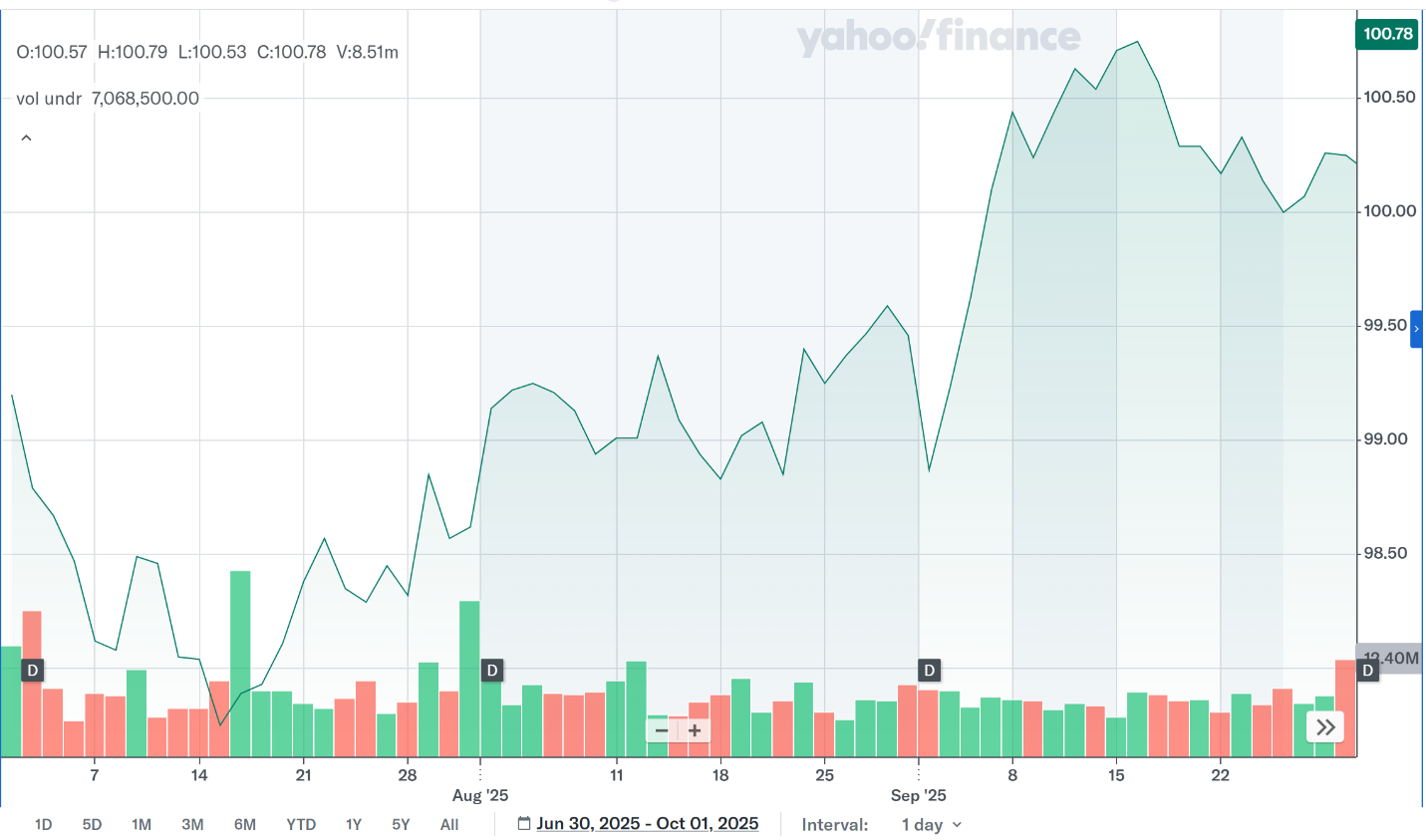

Our description of the market in the first half of the year was ‘Extremes’. Either boring or overly exciting due to the ‘Tarif Tantrum’. Our projection for the third quarter was just ‘Boring’. We couldn’t have been more correct. The graph below is the very definition of Boring.

The largest economic concern this year has been the effects of tariffs. The difference between what has been reported and the lack of worry that investment professionals have couldn’t be farther apart. Tariffs are rarely, if ever, discussed behind the scenes. The theme of the fourth quarter may turn out to be, ‘No News is Good News’.

2025 3rd Quarter Review

The third quarter saw more trade agreements completed and inventories being restocked with post tariff product. The high inflation prediction didn’t happen and demand stayed higher than we expected. Both good developments. We may not be in the clear, but so far, so good.

Demand for credit declined a bit inducing the Federal Reserve to decrease the Federal Lending Rate by a quarter of percent as an insurance policy against rapidly falling consumer demand.

2025 4th Quarter Preview

The stock market tends to drop in late summer and into the fourth quarter. We haven’t seen much of a drop thus far, but wouldn’t be shocked to see more choppiness until we see how Christmas shopping goes.

The Federal Reserve is poised to decrease rates another quarter of a percent if necessary. Another boring quarter would be just fine with us.

Bonds

The Federal Reserve decreased rates as mentioned above. Lower interest rates means gains in bond prices. This led to another quarter of positive correlation to stocks. Both markets increased in value. In other words, the bond market was also boring as shown in the graph below.

US Stocks

While stock prices generally increased steadily in the third quarter, they have become a bit expensive. This can be driven by several factors which include, but are not restricted to, optimism for economic growth, a higher percentage of the S&P 500 is large technology companies, and stock buybacks.

While we are not predicting a short-term market pull back, we would not be surprised to see one. A pull back could be caused by a variety of things including capturing recent profits, low Christmas spending or an unforeseen economic disruption. This means investors should hold stocks and allow our Risk Allocation Models to manage portfolio risk.

International

Last quarter we mentioned that international stocks were interesting due to the high returns in the first quarter. We have not increased our international holdings, which has been the correct decision. We continue to look for reasons to increase our allocation to them, but can’t see an overwhelming reason to do so at this time.

Did You Know?

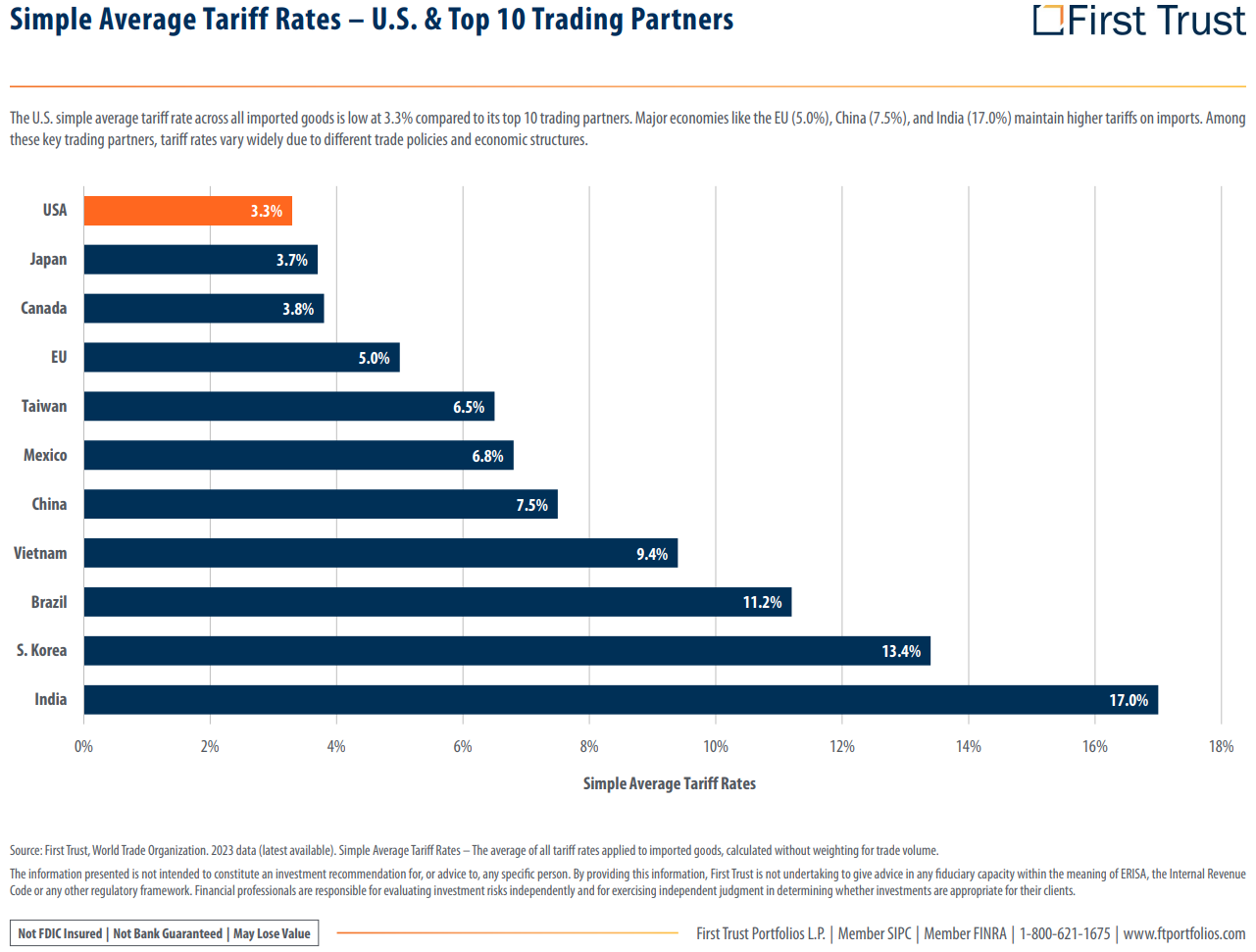

The United State charges less tariffs than any other country. This begs the question, ‘If tariffs are so great for other countries, why are they so bad for the US?’. In other words, ‘Free Trade’, hasn’t been free for the US.

Have you reviewed your retirement strategy this year? We’re here to help.